Preview: FOMC Decision 29 April 2026

Read Time: 3-4 minutes

Next week is a central bank bonanza with five of the eight major central banks set to deliver their decisions.

This will likely be the last meeting for Jerome Powell as Fed Chair as he is set to hand over the reigns to his replacement in May.

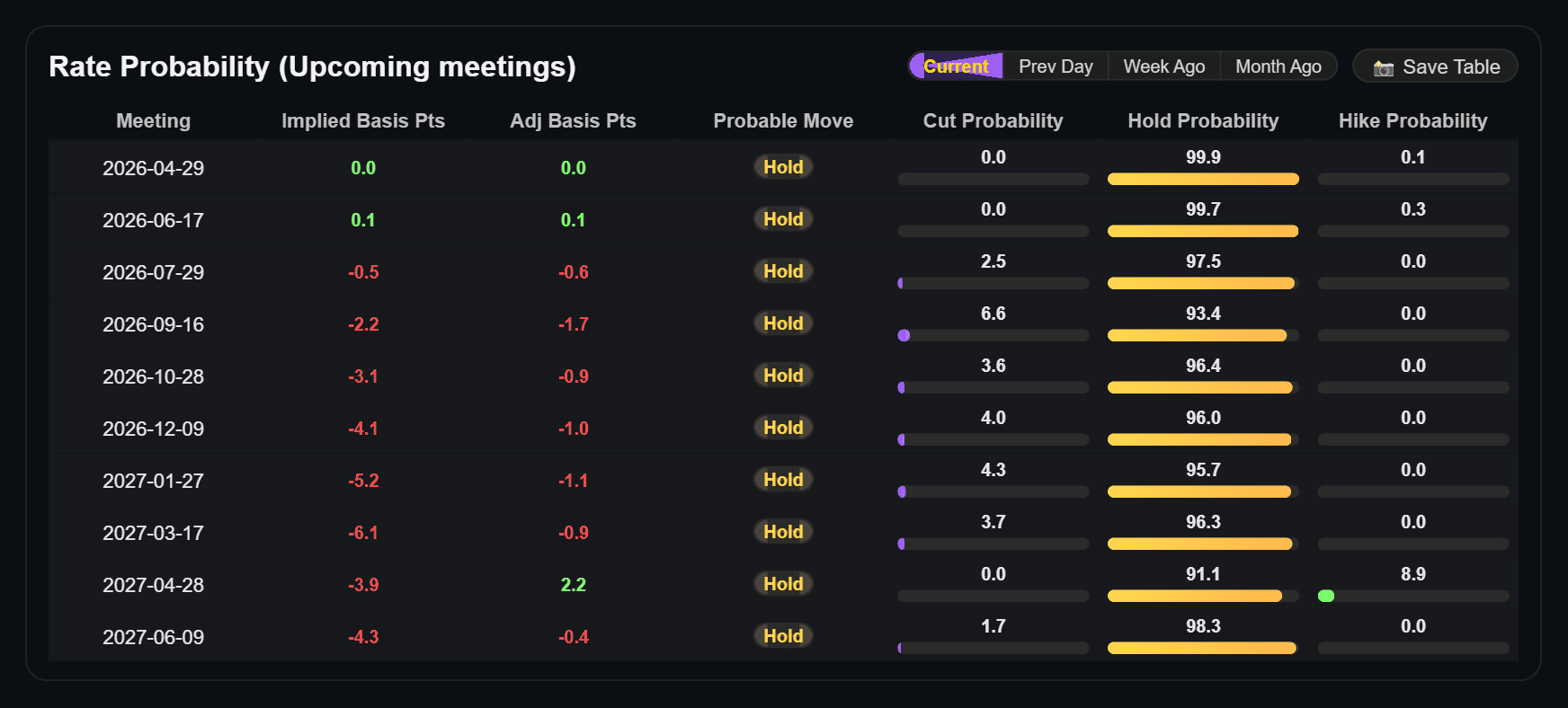

The FOMC is expected to hold policy steady at 3.50% - 3.75% at their meeting next week, in what could well be an uneventful affair.

Rate markets have done some interesting acrobatics since the start of the conflict in the Middle East. Before the crisis, markets were comfortable pricing in two Fed rate cuts by year-end.

Then, just a few weeks after that, they were pricing in 6 basis points of possible tightening. Short-term interest rate markets now anticipate the Fed will keep rates unchanged for the near future.

Given the current uncertainty surrounding energy disruptions, this feels far more realistic, and arguably something the Fed will be comfortable with heading into the meeting.

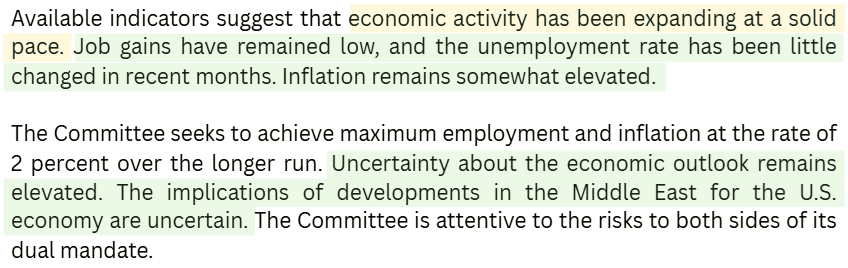

Regarding the statement, expectations are for the Fed to mostly maintain its prior tone and messaging. By stating that job gains have remained low, inflation remains somewhat elevated, and uncertainty about the economic outlook persists.

Given the downward revision to GDP, there is a chance the Fed might adjust its outlook for economic activity to be expanding at a 'moderate' pace, down from the prior 'solid' pace.

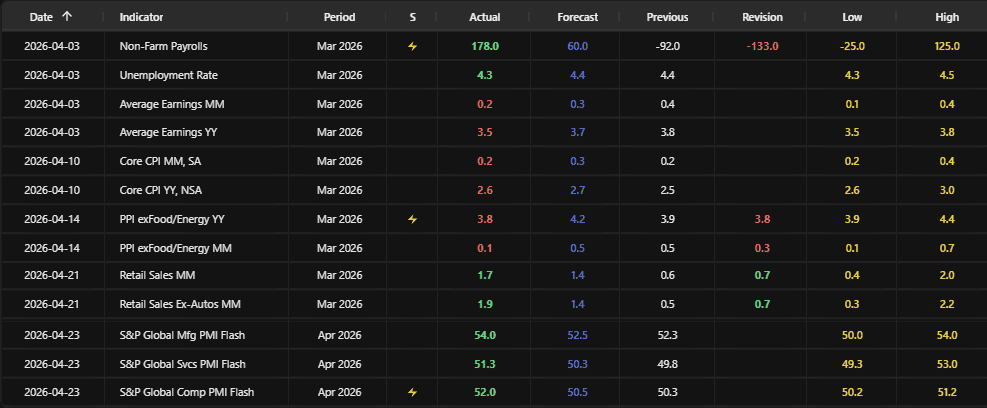

Since their last meeting in March, the economic data has held up okay.

Non-farm payrolls saw a big upward surprise but followed a big contraction in February.

Retail sales held up okay, and April S&P PMIs also printed stronger than expected.

However, the better news for the Fed is that inflation measures have shown very few signs of concern so far.

Core CPI and PPI printed lower than market consensus, with a much smaller-than-expected rise in headline producer prices.

With a hold fully priced in, and the lack of an updated Summary of Economic Projections, the focus for the decision will fall on the statement and press conference.

For the statement, if we see a shift from 'solid' to 'moderate' on economic activity that could see some marginal dovish reactions.

However, it likely won’t be enough to see a strong follow through unless Powell expresses more concern during the press conference.

If Powell emphasizes the continued labour market concerns and worries about negative demand risks from the ongoing Middle East conflict, that could see some dovish repricing.

On the other hand, if he stresses more concerns about inflation risks from the energy shock, or emphasizes willingness to hold rates for longer, it could trigger some hawkish reactions.

However, as this will likely be Powell’s last press conference, he arguably has very little incentive to pre-commit on any policy path as his new successor takes over the reins in May.

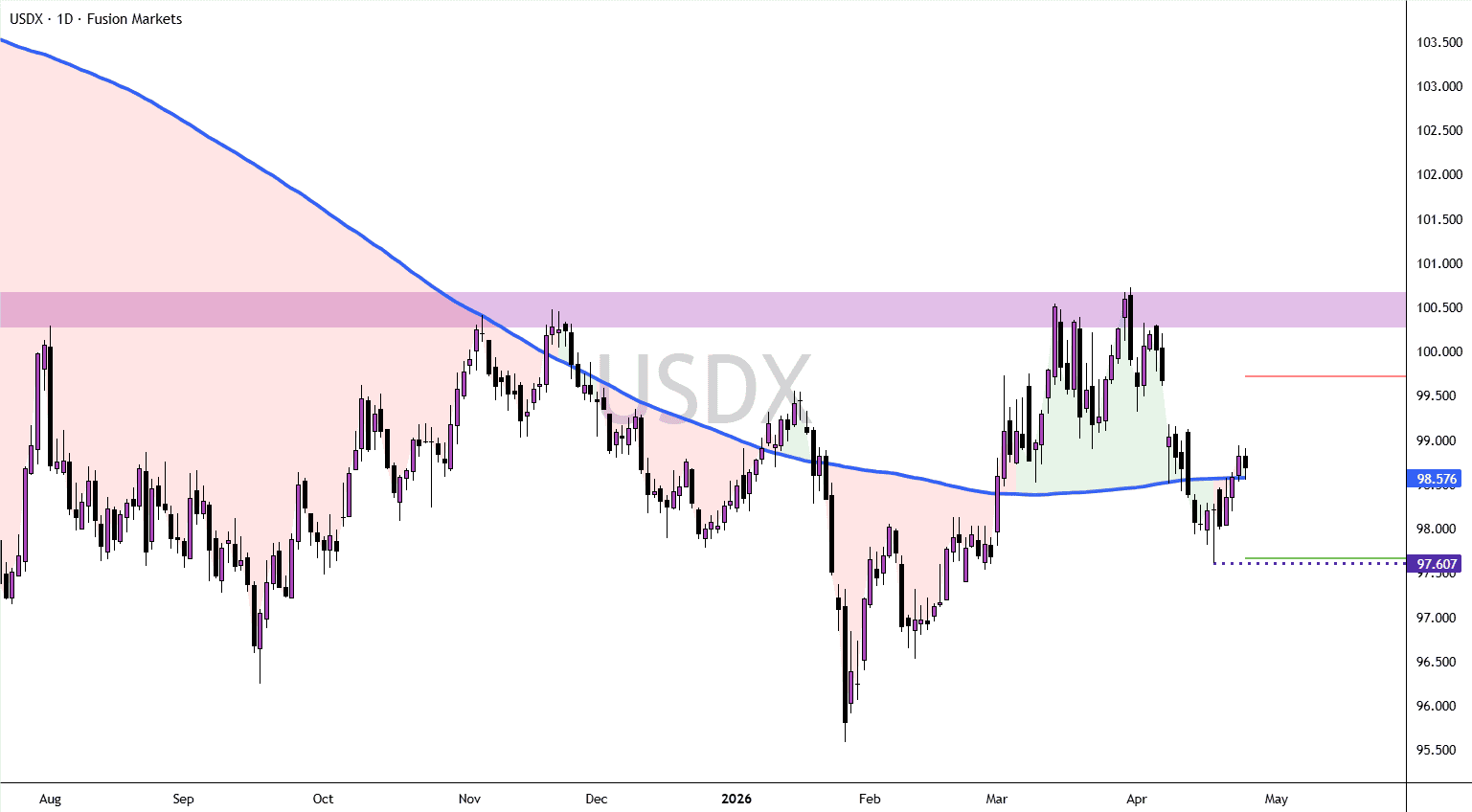

There are a few important levels to keep on the radar for the DXY this week.

The Dollar Index is sitting snug against its 200DMA as we start the new week, which will be an important bias input to watch.

Above that, first implied volatility resistance sits around 99.50, which also has interesting confluence with the gap from 7 April.

Next key support sits around 97.60, which is the swing low from 17 April, and also has confluence with the weekly implied volatility low.

We’ll never share your email with third-parties. Opt-out anytime.

Relevant articles

Preview: Earnings week of 20-24 April